There are many ways to save your home from foreclosure. The first (and most important) step is making the DECISION and COMMITMENT to do so. This will be the fuel that keeps you moving along the way.

There are lots of websites devoted to teaching you about bankruptcy, short sales or walking away as a solution to foreclosure . This isn’t one of them. This website is devoted to helping you understand, uncover and take action against fraudclosure. You may still find it in your best interest to take advantage of one or more of those options. That’s good too. Just know that when you expose your lender’s fraudclosure activities during the process, you will have much better results in whatever action you decide to take.

REMEMBER: If you really don’t believe that it is possible for you to keep your home, then its as good as gone! So before you continue reading, do whatever it is you do to get yourself inspired, motivated or fired-up for success.

Working with an Attorney

What Can I Do to Help Myself?

Yes, I CAN Help Myself!!

Keeping It Real...

Most people are too full of fear and worn down to even consider challenging their lender's fraudclosure. So, don't make the success of this journey dependent on the approval and support of others. In fact, you may want to keep this between you and your immediate family until you've made some significant progress. Know that there are plenty of us out here with an energetic connection to you. We are cheering for you every step of the way!

There are countless tales of people who stood up against their lender and were suddently looked down upon by friends and neighbors who were part of the Misery Loves Company Club. They operate under the notion of "I lost my house, why shouldn't you lose yours" or "I'm stuck with paying thousands of dollars per month on house I can't sell and you should be too!" Did I mention the HOA? They can be a pain too! Just put it all aside because you've got a much bigger prize to win!

Challenging fraudclosure takes courage and lots of it! There will be days when you just know you've caught you lender red-handed only to talk to someone who doesn't understand what you've uncovered or simply thinks it's insignificant. Keep pressing forward anyway. You'll receive signs along the way that you are on the right track and getting closer to your goal.

Keep the faith!!

Putting Together Your Game Plan...

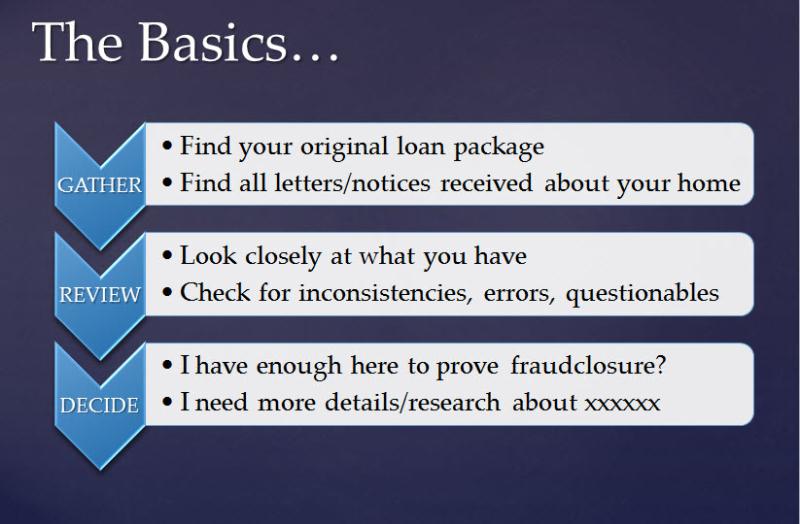

GATHERING Fraudclosure Gems....

Finding my original loan closing package was crucial to the success of my case. In it, I was able to confirm several things:

- That there was the intent to endorse my note in blank from the start

- What the “true/certified” stamp the title company was using in 2006 actually looked like. It was much different than the fake one the default servicer created and stamped on my docs later

- What the endorsement stamp for my lender looked like in 2006 before it was acquired by another institution. It was also much different than the fake one they created and stamped on my docs in 2011

- The names of the players. This seemed insignificant but turned out to be very important later. In 2011, the fraudsters used the names of the 2006 players but messed up by listing their titles wrong…titles that didn’t exist in that department in 2006 but became popular as robo-signing became even more prevalent in 2008, 2009, 2010 and 2011

REVIEWING Fraudclosure Gems...

Take your time and review your documents. There are hints of fraud all looming along the way. I discovered that:

- That my lender transferred the servicing long before notifying me that it was doing so (a clear violation of RESPA)

- That my original lender was just a pretender lender. According to the securitized trust agreement my servicer was actually my lender AND servicer

- My default notices were back-dated several months and signed by the country’s most notorious robo-signers

- There were many notary errors including documents notarized after the date I received them in the mail

- The default servicing company listed the wrong lender on the notice of default

- There was a huge gap in the recorded chain of title

- The wrong lender's name is on my deed

All of these resulted in the lender attempting but being unable to foreclose on my home successfully 4 times.

DECIDING: More Gems to Find?

It was great when my lender took a 10-month hiatus before attempting the foreclosure process all over again. This time, I knew I needed something much stronger to accomplish my goal:

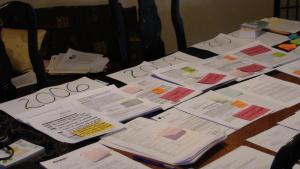

I took what I had and began to segment it like pieces of a puzzle. I laid everything out across my dining room table by year. Next, I color coded my findings…pink for robo-signers, green for bad assignments, blue for problematic substitute trustee docs and yellow for my “gem notes” that I could use in court

From there, I committed 2-4 hours per week to investigating the foreclosure fraud activities of each lender, each default servicing company, each title company and each person who put their “John Hancock” on my documents.

The results were nothing short of amazing! In no time, I was able to find court documents and other verifiable sources that re-connected all the pieces of the fraudclosure puzzle. And I did it all on Google and via the court’s public records!

An attorney can be a wonderful asset in helping you challenge your lender's fraudclosure. However, if you end up with the wrong one, it's much like having a quack doctor --it will make you feel really, really sick.

Many attorneys who formerly specialized in DUI's, traffic tickets and hard-core criminal cases are now in the business of "helping homeowners". There are also the attorneys who have partnered with the foreclosure mills and are involved in as many fraudclosure acts as the lender.

So how do you make sure your attorney is a good fit for your case. Try this:

- Check with your state bar association to see if there are any public complaints

- Check your district and state court records to see how many similar cases they have been successful in

- Google their name or firm name to see what comes up

If all is good, hire them but stay involved.

Copyright 2011-2012 Justice Cashe / NoFraudclosure.com